- 0

.

Football will thrive if the purist’s desire for a meritocracy is wedded with a business approach that heeds the principles of economics, argues Oscar Howie, who contends that Uefa’s Financial Fair Play is a step in the right direction – and that Fernando Torres (left) can’t be value for money.

Football will thrive if the purist’s desire for a meritocracy is wedded with a business approach that heeds the principles of economics, argues Oscar Howie, who contends that Uefa’s Financial Fair Play is a step in the right direction – and that Fernando Torres (left) can’t be value for money.

..

.

.

By Oscar Howie

3 February 2011

Uefa has deemed that football’s financial management requires an overhaul. Its Financial Fair Play (FFP) rules will exclude from its competitions any club running a budget deficit over a rolling three-year period in the long term.

This will eliminate the benefactor investment – the exogenous insertion of cash without a view to its return – that has knocked many clubs out of fiscal balance.

English football’s most prominent benefactor, Chelsea’s billionaire owner Roman Abramovich, illustrated the potential of investment on Monday in spending £50m on Spanish striker Fernando Torres.

Uefa are right to want to prevent such transfers if they are financed from outside the game, not only because they threaten clubs’ solvency, but because competition is being unfairly distorted.

There are two arguments that endorse Uefa’s position. The first is that benefactor investment is damaging for clubs in the long term, as non-performing investments entail debt. The second is that making success exogenous detracts from the purity of the game itself, damaging the integrity that draws us towards sport in the first place.

Uefa’s recognition of the financial argument is its answer to the question, asked for as long as the game has been professional but most vehemently since the advent of Sky and the Premier League, namely can the game thrive, or even survive, as a business? Yes, says Uefa, as long as football clubs adhere to the same economic rules as any other business. If they are right, the endogeneity called for by the purist will be achieved as well.

Football has many of the hallmarks of an economy: trade, competition, finance. It has a bottom line. Football’s problem is that the fundamental plank of economics may be missing: the profit motive. Whilst it has a bottom line, it is not the be-all-and-end-all. Trophies, purists will tell you, are priceless. The ‘revenue’ they yield in prize money is irrelevant; it is the accumulation of achievement, of prestige, an eventual rise to some previously unattained level that confers value upon them.

This is not just true of trophies. What price a win in a local derby? What price a non-league cup run? The purist may be dismayed to hear talk of how much Crawley Town will earn for their journey to Old Trafford in the FA Cup fifth round, but this is symptomatic of the game today.

Whilst it is good that Crawley’s future is secured, the purist’s fascination is with David challenging Goliath, a spectacle not dependent on money for its interest. Is it possible, in this glory-driven context, that the billionaire owners proliferating in English football are here solely for the prize money?

It is possible to accept that the basic aim of football cannot be measured in financial terms without ruling out its potential to function as an economy. This would be fine if the two sides remained detached, in such a way that the business side was conducted with an eye only for the bottom line, and the football side concerned itself only with silverware. This would make owners’ interest in success a function of prize money.

The football side’s money would be one part of a wider budget, properly managed by businessmen that have not left their business sense behind in their previous lives. However, this internal division of labour is not ubiquitous amongst English clubs. We see it at a majority, but a closer look at the Torres transfer will show that it is absent at Chelsea – a scapegoat, but equally a blatant offender. Mr Abramovich wants more than prize money, and his ambition blurs the divide between business and football.

Chelsea’s pretence at achieving fiscal balance – a stated ambition for several years – was undermined on Monday. In the morning the announced a loss of £70.9m for the year to June; in the evening they spent £50m on a new striker and more on a defender.

Their credibility would be salvaged, however, if Torres was shown to be value for money – and not ‘If Ronaldo is worth £80m, then Torres is a bargain at £50m’ value, or even, ‘If Andy Carroll…’ value.

That is the language of football, not business. If football wants to be a legitimate, robust business, it must adhere to economic principles. The question then becomes this: is Torres’s present value – the expected return on his performance for all time – greater or less than the £94.2m (£50m plus £44.2m wages over five years) that he will cost Chelsea over the next five years?

Torres’s present value is the value that he is expected to add to Chelsea in the next five years. It is the difference between Chelsea’s expected revenue with him and Chelsea’s expected revenue without him.

This is calculated by adjusting the probability of the potential set of outcomes to take into account Torres’s presence.

The club’s major revenue streams are prize money and television money from the Premier League (PL) and Champions League (CL).

This year, Chelsea are faced with the prospect of missing out on CL qualification for 2011-12 if they fail to finish in the top four of the PL – and it is possible that their decision to buy the Spaniard was motivated by this fear.

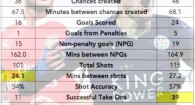

Based upon a fourth-placed finish this season, four wins in the group stage, and a run to the quarter-final next season, the competition would be worth £23.3m to the bottom line, or thereabouts.

Let’s say that without Torres, Chelsea have a 60 per cent chance of achieving this, and that with Torres they have a 90 per chance. Yes, the numbers are subject to debate, depending on amongst other things how you judge Chelsea’s squad and the claims of Tottenham, but a 30 per cent swing is very generous to any individual in a team sport.

This makes Torres’s expected value for 2010-11 to be £6.99m, or 30 per cent of £23.3m.

Moving beyond this season, Torres’s value is again determined by how he alters the probability that the club will achieve a given amount of success.

The model employed here is a tripartite four-year performance measure. Chelsea could win the PL and CL double each season, and let’s assume this is impossible without Torres, and a 10 per cent likelihood with him; or they could average second place in the PL and reaching the CL quarter-final (80 per cent chance with Torres, 50 per cent without him); or they could finish fifth each season and hence not reach the CL at all (10 per cent chance of this with Torres, 50 per cent without him). These are generous percentages for the influence of one man.

Over four years, this analysis values Torres at £60.5m, with the probabilities generous both to Torres and to Chelsea, maximising Torres’s potential to add value.

In addition to the £7m from this year, this makes his present value £67.5m. This is a £26.7m shortfall against the £94.2m expenditure. (See the graphic below for a fuller explanation of the calculation. Click on it, or click here, to enlarge it.)

Chelsea’s decision to buy Torres was not economically sound: they will not recoup their investment.

Chelsea’s decision to buy Torres was not economically sound: they will not recoup their investment.

Of course, investment is a crucial part of all economies, including football, but elsewhere it remains tied to the profit motive. Projects that cost more than their present value are not invested in. Transfers that flaunt this economic rule happen for two related reasons: because there is no division between the finance and the football, and because the investment is not put in to be regained.

Oligarchs have made their profits; now they want trophies. The two exist in different contexts: one pays for the other, with football accruing the losses.

Football is not operating like any other economy: its costs are not linked to its revenues. Torres was paid for by Russian oil, not by the Stamford Bridge faithful, Sky’s subscribers, or Uefa’s European competition.

Non-football money is not a panacea, as was shown by the financial results Chelsea released on the very same day as the Torres signing.

Having a billionaire in your corner does not keep you in the black; it means that you can afford to go in to the red.

Chelsea are not the first club to finance their spending from resources beyond their own revenues. Jack Walker’s approach in taking Blackburn to the title in 1995, spending millions of his own money on players such as Chris Sutton and Alan Shearer, provided a template for success.

It might be argued that private money has always been in football, since the very early days of professionalism. This is undoubtedly true, but in the past private money was invested – in the true sense – with an eye to recovering it later, rather than simply spent.

Deficit spending in football is a modern phenomenon: of the 64 instances of British clubs entering administration (up to 2009), 52 have been since 1995.

The problem, in the eyes of the economist – as Liverpool themselves discovered in the years of wrangling that preceded the NESV takeover, and mortgage lenders the world over discovered in 2008 – is that unbacked debt is not easy to sell, and eventually becomes too expensive to service, leading to default and closure.

When Mr Abramovich has had enough, what then? For Lehmann, read Chelsea.

The problem, in the eyes of the purist, is that the basis of success becomes exogenous to the game. Money made elsewhere is introduced into the game and acts to distort its competitive outcomes.

A deluge of Torres goals would cost Tottenham a place in the Champions League, and the explanation would be an exogenous mid-season intervention. This is not the competition that we seek in sport.

Uefa, in instituting FFP, has accepted that there is a problem and has ruled that clubs must break even from 2011-12, with a few caveats.

Sadly, it has taken the economic perspective to bring about the change that the purists have been calling for for years. It will not make football a level playing field in the eyes of an egalitarian, but neither should it: those that succeed should be rewarded, and are then in the privileged position to invest that reward in their own future. Here, the competition that economics relies upon is a natural counterpart to football.

Business will remain a part of football for as long as it generates billions of pounds every year. This is not necessarily a bad thing. The sport will thrive as a meritocracy.

It is widely agreed that the financially motivated Premier League is the best league in the world. Eradicating the exogenous business elements and thereby re-equating costs and revenues, however, means that there is the prospect of success becoming endogenous once again. That at least should make the purist smile.

.

More stories mentioning Chelsea

(including this on persistent excuses about losing pots of dosh)